| by Glenn J. Downing, MBA, CFP® |

How to get a big pay hike

If you want a big pay hike, sometimes the only way you’re going to get it is by jumping ship to a new employer who values your skill set and experience and is willing to pay for it. People will make several job changes over a working lifetime for this reason.

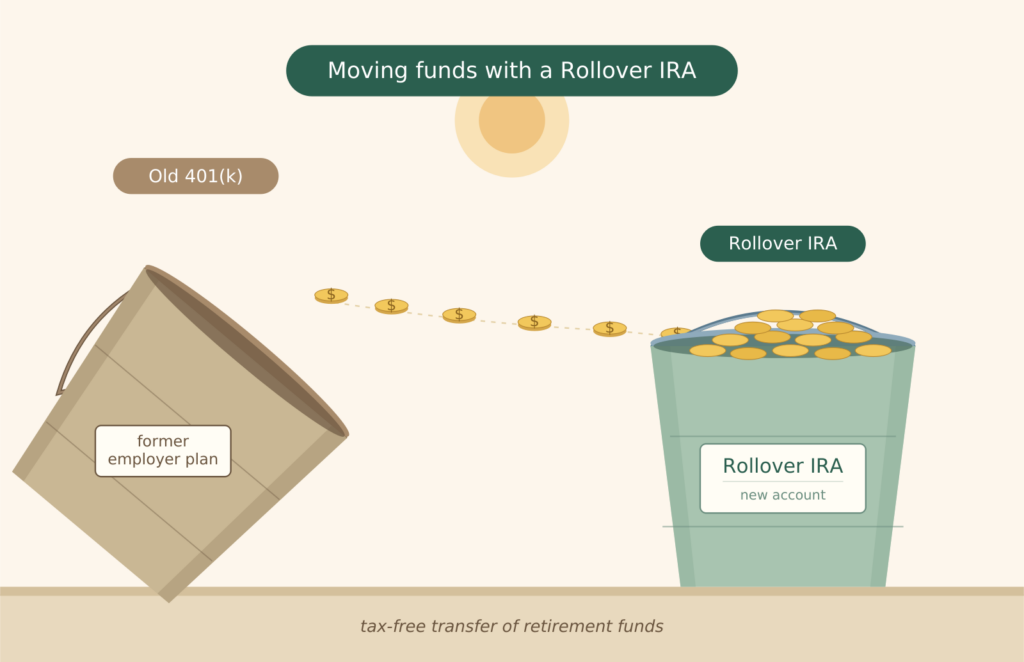

What do I do with my old retirement plan?

A default answer with many advisers is to tell people to move the funds to a rollover IRA. Often good advice, but not always in your best interests. Let’s consider:

Reasons TO DO a Rollover IRA

- A huge range of investment options, including cryptocurrency ETFs. This includes shares of start-up companies that could potentially explode. Employer plans tend to offer nothing much beyond the plain vanilla large/mid/small cap funds.

- RIA fees will be higher than what you pay in your work retirement account. But an IRA account with a firm such as CameronDowning also gets you a personal advisor who knows you and your circumstances. The fee you pay acts as a sort of retainer, to have a personal financial advisor always accessible.

- Distributions from your IRA are easy. We can set them up to be periodic with electronic transfer to your checking account.

Reasons Why NOT to do a rollover IRA

- If your plan at work is covered by ERISA legislation – typically a profit sharing or 401K – it has complete creditor protection, no matter the balance. An IRA will have limited creditor protection.

- Loans are permitted from employer plans. No loans ever from IRAs.

- Early withdrawal penalties of 10% apply to retirement plans before age 55. It is age 59½ for IRAs. So if you are age 55, separated from service, and rolled your retirement funds into an IRA, you’ve just given yourself 4½ years of 10% withdrawal penalties.

- Higher fees paid to a Registered Investment Advisory firm rather than within the employer plan.

- If you have employer stock in your plan, consider a distribution to an individual account. You’ll be taxed now on the basis of that stock, but when you distribute you’ll pay capital gains tax — much lower than the ordinary income taxation on IRA distributions.

- You May Not Have a Choice

In some employer plans if you are no longer employed there they want you to get your money out right away. In others, they allow you to continue participating in the plan into retirement or even for life. Knowing what you have and how it works is crucial for making a wise decision.

Here at CameronDowning we have a fiduciary responsibility to help you weigh all these factors so that you can make an informed decision that is in your best interests.

Here are some other articles you may find helpful”